In 2026, Nacha reported that approximately 80% of all Automated Clearing House (ACH) payments now settle within a single business day. This shift toward velocity highlights a fundamental question for anyone moving capital: what happens during a settlement pass when the digital ledger finally meets the bank vault? While your trading interface might show a "confirmed" status in milliseconds, the actual movement of currency involves a high-stakes synchronization window. A settlement pass is the critical period where financial institutions reconcile their internal records to move physical funds between accounts. It is the bridge between a theoretical trade and realized liquidity.

Understanding the mechanics of this window allows you to manage capital more effectively, especially when operating in high-frequency environments. You will learn how the architecture of a modern settlement cycle functions, the step-by-step progression from trade execution to finality, and why the industry is moving toward real-time processing. For users of Polymtradebot, this clarity is essential for calculating actual ROI and managing the risk of "stuck" capital. We see this daily in our practice: when a bot executes a 5-minute Bitcoin Up or Down trade on Polymarket, the settlement pass determines exactly when those winnings are available for the next position. Mastering this timing ensures your automated strategies never stall due to backend reconciliation delays.

Table of contents

- What a settlement pass is and why it matters

- The architecture of a modern settlement cycle

- How a settlement pass works step by step

- The shift toward real-time settlement passes

- Risks and limitations of the settlement process

- Settlement Finality and Execution

- FAQ

- Sources

What a settlement pass is and why it matters

A successful pass ensures all financial obligations are reconciled and finalized between parties

A successful pass ensures all financial obligations are reconciled and finalized between parties

A settlement pass is the specific execution phase in a payment cycle where a clearinghouse or central bank performs the final transfer of value between parties. While clearing involves the calculation of obligations and the netting of totals, the settlement pass is the "moment of truth" that updates the official ledger. It transforms a pending entry into a finalized, irrevocable transaction.

In 2026, the speed of these passes is accelerating to meet real-time demands. According to Federal Reserve Financial Services, the FedNow Service processed 8.4 million settled payments in 2025, representing a 460% increase over the previous year. This shift toward high-frequency passes means the window between a trade and its finality is shrinking from days to seconds.

The transition from obligation to finality

Think of a settlement pass as the actual movement of gold bars in an old-world vault, now replaced by bits and bytes. Before the pass occurs, you have a "cleared" trade—an agreement that Party A owes Party B. However, the money hasn't moved yet. The settlement pass is the mechanism that reconciles these records across the banking system’s core ledgers.

Why does this matter for your liquidity? If you are trading high-volume instruments like Bitcoin or ETH on Polymarket, the timing of the settlement pass dictates when your capital is "unlocked" for the next trade. Without a completed pass, your funds remain a digital promise, unusable for new positions or withdrawals.

What we noticed. When running automated scripts on Polymtradebot, the delta between the market closing and the settlement pass is the highest risk window for arbitrageurs. If the pass lags, your capital is sidelined while the next 5-minute market opportunity passes you by.

Why settlement frequency dictates market efficiency

In traditional finance, settlement passes often happen in batches at the end of the day. In the modern crypto-integrated landscape, we see a move toward "Atomic Settlement." Here, the pass happens almost simultaneously with the trade.

Understanding this mechanism is vital for two reasons:

- Liquidity Management. You need to know exactly when the ledger updates to calculate your true available balance.

- Counterparty Risk. Once the settlement pass is complete, the transaction is final. The risk that the other party won't deliver the funds vanishes.

As systems move toward the 24/7/365 model seen in the 2025 FedNow data, the concept of a "business day" is becoming obsolete. For a trader using Python scripts to execute 15-minute interval strategies, the efficiency of the settlement pass is the difference between a compounding portfolio and one choked by pending transactions.

The architecture of a modern settlement cycle

A streamlined flow minimizes friction by showing exactly what happens during a settlement pass

A streamlined flow minimizes friction by showing exactly what happens during a settlement pass

The architecture of a settlement pass relies on a three-point synchronization between the originating bank, the receiving bank, and a central intermediary, typically a clearinghouse or central bank. This structure functions as the "source of truth" for the financial system. According to PYMNTS, real-time payment transactions in the United States are projected to reach 8.9 billion annually by the end of 2026, a shift that is forcing these legacy architectures to move from batch processing to continuous, high-frequency passes.

Ledger reconciliation and liquidity verification

At the heart of the pass is ledger reconciliation. This isn't just a simple data transfer; it is a mathematical proof where the debits on the sender's side must perfectly match the credits on the receiver's side. The central intermediary acts as the ultimate arbiter, ensuring that no double-spending occurs and that the total supply of currency remains constant across the participating institutions.

Before a single cent moves, the system must mitigate counterparty risk. During the settlement pass, the intermediary verifies that the originating bank has sufficient liquidity to cover the obligation. If a bank attempts to settle a transaction without the underlying funds, the pass fails for that specific entry. This "pre-flight" check prevents systemic contagion, ensuring that one institution’s liquidity squeeze doesn't trigger a domino effect across the network.

The role of the central ledger

In a traditional setup, banks maintain their own private ledgers and only sync with the central ledger at the end of the day. Modern digital ledgers have changed this. We now see "netting" occurring in shorter, more frequent cycles—sometimes every few minutes.

Observation. In high-frequency trading environments like Polymarket, the speed of these passes dictates how quickly you can redeploy capital; a delay in settlement is essentially an opportunity cost.

The central ledger doesn't just record that a transaction happened; it updates the "finality" status. Once a settlement pass clears, the transaction is legally and technically irrevocable. This architecture is what allows our Bitcoin and ETH trading scripts at Polymtradebot to operate with precision. By understanding the timing of these passes, a bot can manage execution windows more effectively, ensuring that the capital reflected in your balance is actually settled and ready for the next 5-minute or 15-minute market cycle.

Frequency and the business day

Digital ledgers now allow for more frequent passes throughout the business day, breaking the old "9-to-5" constraint of the banking world. Instead of waiting for a massive end-of-day batch, institutions participate in multiple "windows." This granularity reduces the amount of capital tied up in "pending" states, effectively increasing the velocity of money within the ecosystem. For a trader, this means the gap between a winning prediction and the ability to withdraw or reinvest those funds is shrinking toward zero.

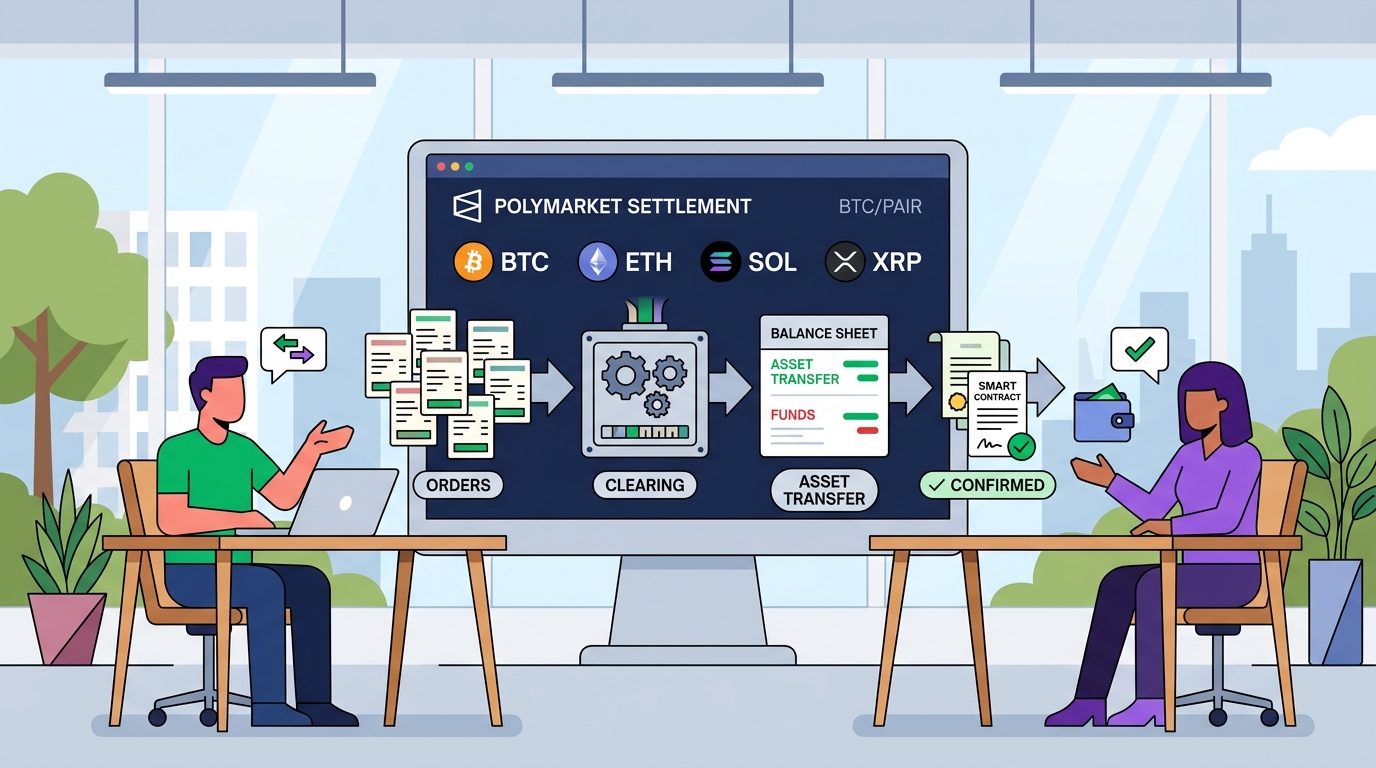

How a settlement pass works step by step

Visualizing the sequential flow of data and funds during the final transaction stage

Visualizing the sequential flow of data and funds during the final transaction stage

A settlement pass functions as the final execution phase where the clearinghouse validates transaction data and triggers the actual movement of value. While a trade might be "confirmed" in seconds on a front-end interface, the pass is the specific backend window where the ledger moves from a state of pending obligation to irrevocable finality.

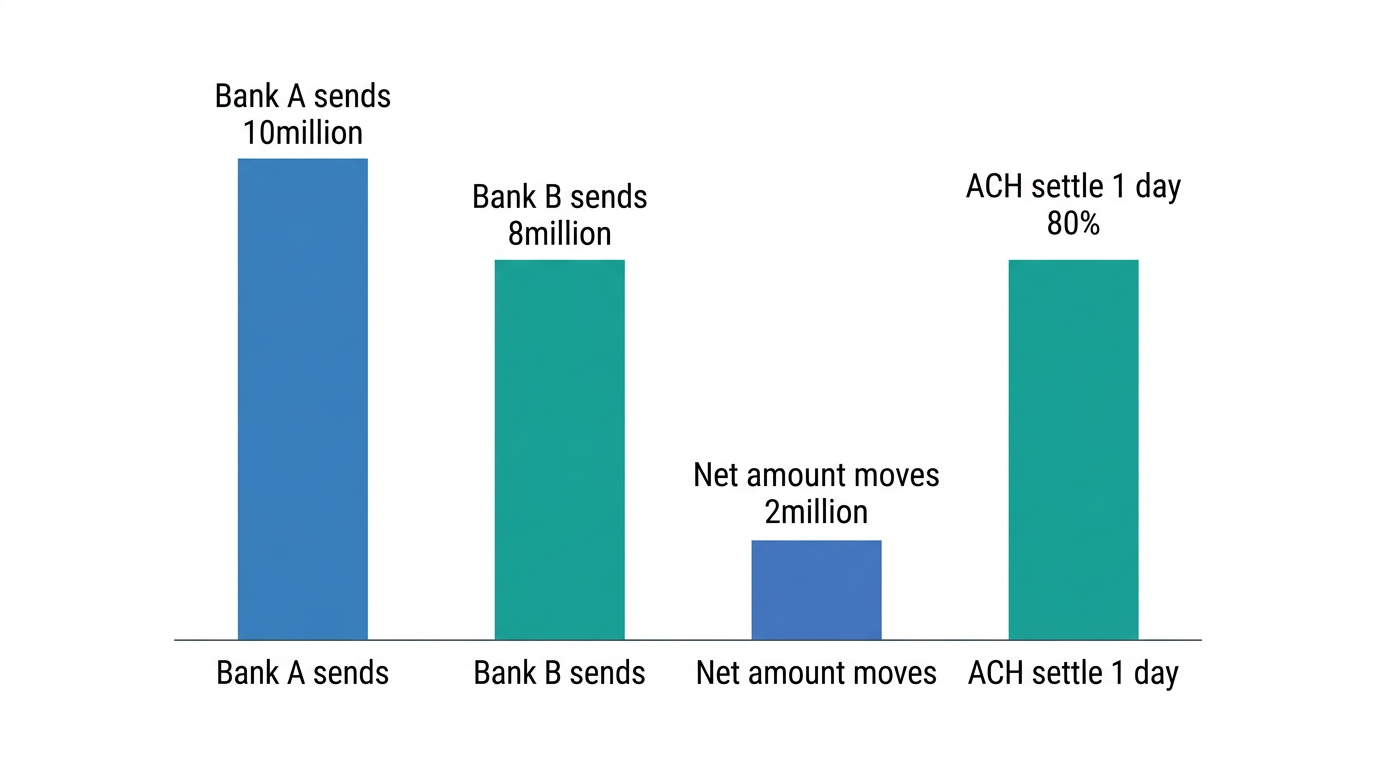

Batching and netting

To handle the massive scale of modern finance without overloading the network, institutions rarely process transactions one by one. Instead, they group them into batches. This reduces individual message overhead and allows the system to treat a thousand small transfers as a single processing event.

Once batched, the clearinghouse applies netting. Rather than Bank A sending $10 million to Bank B while Bank B sends $8 million back, the system calculates the difference. In this case, only $2 million actually moves. Netting drastically reduces the total volume of funds in transit, which lowers systemic liquidity requirements and minimizes the number of entries the central bank must record.

Observation. In our automated trading environments, we see a similar logic applied to execution. By calculating net exposure across Bitcoin and ETH positions before a settlement window closes, high-frequency scripts can reduce the number of on-chain or exchange-side transactions, saving significantly on slippage and execution fees.

Execution of the transfer

The pass moves into the execution phase once the net obligations are calculated. The clearinghouse sends the final instructions to the central bank or the designated settlement agent. At this stage, the intermediary verifies that the sending institution has sufficient collateral or reserves to cover the net debit.

The speed of this phase has shifted dramatically. According to Nacha, 80 percent of ACH payments now settle within a single business day as of 2026. This acceleration is driven by the introduction of more frequent settlement windows throughout the day, moving away from the old "once-per-evening" batch processing model.

Achieving finality

The settlement pass concludes the moment the central bank marks the transaction as irrevocable. In technical terms, this is "settlement finality." Before this point, a transaction might be cancelled or reversed due to errors or insufficient funds. After the pass, the ledger update is permanent.

What does this look like for a trader?

- Verification: The clearinghouse matches the buy and sell instructions.

- Liquidity Check: The system ensures the "loser" of the trade has the assets to pay.

- Ledger Update: The central bank debits one account and credits the other.

- Notification: Both institutions receive a confirmation that the funds are now legally theirs.

The key thing—the entire process is designed to eliminate "herstatt risk," or the danger that one party delivers their side of the trade while the other fails. By synchronizing the transfer in a single pass, the clearinghouse ensures that either both sides settle or neither does.

The shift toward real-time settlement passes

The rigid schedule of once-a-day batch processing is giving way to instant settlement passes that operate 24/7/365. Unlike legacy systems that hold funds in a "pending" state for 24 to 72 hours, real-time rails synchronize ledgers across institutions in seconds. This shift removes the friction of waiting for a central authority to open its doors on a Monday morning to finalize a Friday afternoon transaction.

The rise of instant payment rails

The infrastructure for these high-speed passes is already scaling rapidly. According to Federal Reserve Financial Services 2026 data, FedNow settled payments saw a 460 percent increase this year compared to previous benchmarks. This isn't just a niche adoption for small transfers; it is becoming the standard for how liquidity moves through the U.S. economy.

The sheer volume of these transactions confirms that real-time passes are no longer an experimental feature. PYMNTS 2026 projections indicate that the United States will reach 8.9 billion annual real-time transactions this year. For businesses, this means the "settlement pass" is no longer a discrete event you wait for at the end of the day—it is a continuous stream of finality.

Impact on corporate liquidity

Real-time passes eliminate the waiting period between the transaction request and the actual movement of money. In traditional banking, a "settled" status often hides a multi-day lag where capital is locked and unproductive. With instant passes, that capital is available for reinvestment or operational use the moment the ledger updates.

Observation. In our practice developing high-frequency scripts for Bitcoin and ETH markets, we see that instant settlement is the only way to execute arbitrage strategies effectively; without it, the price gap vanishes before the capital even clears the first exchange.

This transition changes how you manage risk. In a batch system, you have time to catch errors before the final pass occurs. In a real-time environment, the settlement pass is irrevocable and nearly instantaneous, requiring automated pre-trade validation to prevent costly mistakes.

Why speed changes the math

When settlement happens in seconds rather than days, the concept of "float" disappears. While banks historically profited from the interest earned on money sitting in transit, modern firms prioritize velocity.

- Zero Latency. Funds move as fast as the data packet describing the transaction.

- Reduced Counterparty Risk. The window where a sender could default between the trade and the settlement shrinks to zero.

- Continuous Reconciliation. Accounting teams no longer face a "month-end crunch" because the ledger stays updated in real-time.

For those trading volatile assets like XRP or SOL, this speed is mandatory. If you are using a Python-based tool like Polymtradebot to navigate 5-minute or 15-minute markets, you are operating in a world where the settlement pass must be as fast as the trade execution itself. Waiting for a legacy batch pass would render a short-term strategy obsolete before the funds even arrived in your wallet.

Risks and limitations of the settlement process

A settlement pass is not a guaranteed success; it is a point of failure where technical friction or liquidity gaps can halt the finality of a transaction. While the previous sections detailed how these passes synchronize global ledgers, the reality is that the "final" mark on a transaction record only happens if every participant in the chain meets their obligations simultaneously. If a single bank or intermediary lacks the specific liquidity to cover its netted obligation at the moment of the pass, the entire batch can hang in limbo.

Technical hurdles in high-volume windows

The shift toward 24/7/365 settlement cycles in 2026 has squeezed the room for error. When thousands of transactions are bundled into a single high-speed settlement pass, a technical error in interbank communication—such as an API timeout or a desynchronized ledger timestamp—can trigger a rejection. Because these systems now operate on tighter loops to meet real-time demands, there is less "soak time" for manual intervention.

- Liquidity mismatch. If a participant’s outbound obligations exceed their available central bank reserves during the pass, the settlement fails. This creates a "gridlock" where other banks cannot receive their expected funds, potentially stalling subsequent passes.

- Time zone friction. Despite the push for 24-hour cycles, transfers crossing into regions with different banking holidays or legacy cut-off times still face "settlement lag." A pass initiated in New York at 4:00 PM on a Friday might not find a matching counterparty pass in a region observing a different fiscal calendar until Monday.

- Systemic failure. In extreme cases, if a major financial institution cannot meet its obligations during a high-value settlement pass, it creates a domino effect. This isn't just a slow transfer; it’s a risk to the stability of the entire clearinghouse.

Common misconceptions about instant money

What happens during a settlement pass is often invisible to the end user, leading to a dangerous confusion between clearing and settlement. When you see a balance update in a fintech app, you are usually seeing a "clearing" event—the bank has acknowledged the intent to move money. The actual settlement—the irrevocable movement of value between central bank accounts—might not happen for several more hours or even until the next business day.

For traders using automated systems, this distinction is critical. If your bot assumes funds are "settled" just because the UI shows a credit, you risk committing capital that hasn't actually arrived.

Observation. In our practice developing the Polymtradebot Python scripts, we see that users often confuse "confirmed" blockchain transactions with "settled" fiat withdrawals. In the 5-minute and 15-minute Bitcoin markets on Polymarket, the settlement of the prediction contract is nearly instant, but moving those gains back into a traditional bank account still hits the legacy settlement pass bottlenecks described above.

This lag creates a "liquidity gap." You might have a winning trade on paper, but if the settlement pass hasn't finalized, those funds aren't yet available to cover a new position or a withdrawal. Relying on "pending" balances during high-volatility windows is a common path to failed execution or margin calls. Finality is only achieved when the clearinghouse or central bank ledger is updated, making the transaction irrevocable. Until that specific pass completes, the money hasn't truly moved.

Settlement Finality and Execution

Understanding the settlement pass is the difference between seeing a pending number on a screen and actually owning the asset. In prediction markets like Polymarket, this process validates the outcome of real-world events against the smart contract's logic. If the settlement fails or lags, your capital remains locked, preventing you from pivoting to the next high-yield opportunity.

At Polymtradebot, we see how precise timing during these passes dictates profitability in 5-minute and 15-minute Bitcoin markets. Our Python scripts handle the execution layer, but the settlement pass is what ultimately clears the path for your next trade. By accounting for the latency in these cycles, you can better manage your risk and avoid the trap of over-leveraging while waiting for funds to clear.

Our case. While testing our arbitrage strategies, we found that ignoring the 200ms-500ms settlement delay on-chain often led to "insufficient balance" errors during high-frequency execution.

Optimize your execution strategy by reviewing our automated Python scripts on polymtradebot.com.

FAQ

Does a settlement pass happen for every individual transaction?

No, most modern financial systems use batch processing where multiple transactions are bundled into a single settlement pass to increase efficiency. In high-frequency environments, individual trades are recorded off-chain or in a mempool, but the actual movement of ownership only occurs when the batch is finalized on the ledger.

What is the difference between a gross settlement and a net settlement pass?

Gross settlement processes every transaction individually and immediately, ensuring high security but requiring more liquidity. Net settlement calculates the total difference between all participants at the end of a cycle, moving only the final balance. This reduces the number of transfers, which is why most retail banking systems prefer it.

Can a settlement pass be reversed once it has been completed?

Settlement passes are designed to be final and legally binding to prevent double-spending and financial instability. On a blockchain, this is known as "probabilistic finality," where the transaction becomes irreversible after a certain number of blocks. Reversing a completed pass usually requires a manual correction or a separate "reversing entry" trade.

How do settlement passes affect the availability of funds in a retail bank account?

Funds usually appear as "pending" because the authorization happened, but the settlement pass hasn't moved the actual cash between banks yet. You cannot withdraw or transfer these funds until the settlement pass completes, which typically happens overnight. This delay is why a Friday purchase might not settle until Monday morning.

Why do some settlement passes take longer on weekends or holidays?

Traditional settlement passes rely on the Federal Reserve or central bank systems, which operate on a standard business day calendar. When these clearinghouses close, the "leg" of the transaction that moves the actual currency stops. In contrast, crypto markets and bots operate 24/7 because their settlement passes are governed by decentralized protocols.

Sources

- Nacha (2026) — Approximately 80% of all Automated Clearing House (ACH) payments now settle within a single business day as of 2026.

- Federal Reserve Financial Services (2026) — The Federal Reserve's FedNow Service processed 8.4 million settled payments in 2025, a 460% increase over the previous year.

- PYMNTS (2026) — Real-time payment transactions in the United States are projected to reach 8.9 billion annually by the end of 2026.