According to Mordor Intelligence, in 2026 the Asia-Pacific region is projected to be the fastest-growing chatbot market with a 24.71% compound annual growth rate. This surge highlights a massive shift toward localized automation, yet many traders remain tethered to default settings that ignore regional volatility and liquidity shifts. If you are running a standard script on Polymarket, you are likely missing out on arbitrage opportunities that exist only during specific timezone overlaps or within regional asset pairs like XRP or SOL. Learning how to customize the bot source code for new markets is the difference between a generic execution and a precision tool that captures gains while others are asleep.

In our practice at Polymtradebot, we have found that hard-coded slippage tolerances often fail when moving from high-liquidity Bitcoin 5-minute markets to emerging regional tokens. By adapting your Python scripts, you can implement localized risk management and adjust execution logic to match the specific order book depth of new trading pairs. You will learn the exact technical requirements for modifying Python-based trading logic, how to structure your API calls for regional endpoints, and the specific steps to validate your deployment using paper trading mode. This allows you to scale your strategies into high-growth zones without risking capital on unoptimized code.

Key Takeaways

- The Asia-Pacific region will see a 24.71% CAGR in chatbot tech by 2026, signaling a major shift toward automated regional trading.

- Customizing source code enables traders to adapt slippage and liquidity parameters for volatile assets like SOL and XRP.

- Use paper trading mode to simulate localized market conditions before deploying live capital.

- Regional expansion requires modifying Python execution scripts to handle specific timezone liquidity shifts.

Table of contents

- What market customization is and why it matters

- Technical requirements for code modification

- How to customize the bot source code for new markets: Step-by-step

- Adapting strategies for regional growth

- 5 mistakes that break market expansion

- Checklist: Verifying your customized deployment

- Conclusion

- FAQ

- Sources

What market customization is and why it matters

Adapting code to local user behavior ensures your bot resonates with global audiences

Adapting code to local user behavior ensures your bot resonates with global audiences

Market customization is the process of reconfiguring the bot’s core logic—specifically asset pairs, API endpoints, and execution parameters—to trade niche Polymarket categories beyond the default Bitcoin and Ethereum sets. For a script like Polymtradebot, this doesn't mean a total rewrite. Instead, you are adjusting the Python source code to point at specific contract addresses and liquidity pools that match your chosen market's profile.

Specialization is becoming the baseline for automated trading. In 2025, Gartner predicted that 40% of enterprise applications will feature task-specific AI agents by 2026, a massive jump from less than 5% in 2025. This shift toward "task-specific" logic applies directly to prediction markets. A bot tuned specifically for SOL or XRP volatility performs better than a generalist tool because it accounts for the unique volume spikes and participant behavior of those specific communities.

Expanding beyond Bitcoin and Ethereum

While Bitcoin and ETH offer the highest volume, they also attract the most sophisticated competition. Customizing the source code allows you to pivot toward high-growth assets like Solana (SOL) or Ripple (XRP). These markets often exhibit different momentum patterns. By modifying the market_id and clob_endpoint in your configuration, you can deploy the same arbitrage or trend-following logic to "under-fished" waters where the spread between "Yes" and "No" shares might stay wider for longer.

What we noticed. In lower-liquidity markets like XRP, a standard 5-minute execution window often leads to high slippage because the order book isn't deep enough to absorb rapid-fire trades without moving the price against you.

Optimizing for liquidity and intervals

Customization is often a play for lower slippage. When you target niche markets, you must align the bot’s heartbeat with the market's natural rhythm.

- 5-minute intervals: Best for high-cap assets like BTC where price discovery is instantaneous and liquidity is deep.

- 15-minute intervals: Often more effective for SOL or emerging tokens. The longer window allows liquidity to replenish on the Polymarket order book, ensuring your automated execution doesn't eat its own profit through price impact.

Adjusting these intervals in the source code prevents the bot from "chasing" ghost liquidity. If you trade a 5-minute market with a bot set to a 1-minute polling rate, you risk triggering false signals based on temporary price noise. Customizing the code ensures the bot only fires when the statistical edge is actually present in that specific asset's lifecycle.

Technical requirements for code modification

Ensure your development environment meets the specific dependencies required for seamless local deployment

Ensure your development environment meets the specific dependencies required for seamless local deployment

Modifying the Polymtradebot source code requires a stable development environment that mirrors the production environment where your trades execute. According to McKinsey & Company, in 2025, 88% of organizations now use AI in at least one business function to drive growth, a trend that underscores the necessity of robust technical foundations when automating financial decisions. Before you adjust logic for new assets like SOL or XRP, you must ensure your local machine can handle the specific asynchronous demands of the Polymarket API.

Development environment setup

The bot runs on Python 3.9 or higher. We rely on this versioning because the script utilizes specific dictionary merging and type hinting features that older versions lack. You will need to install the polymarket-sdk and web3.py libraries to manage the interaction with the Polygon network.

Verify your setup by running a simple version check in your terminal: python --version. If you are targeting 5-minute or 15-minute intervals, your system clock must be synchronized via NTP to avoid signature mismatches when sending orders to the exchange.

What we noticed. When expanding to high-volatility markets like SOL, even a two-second drift in your system clock can cause the Polymarket API to reject your transaction nonce, leading to missed execution windows.

API credentials and security

To interface with the Polygon network, you need a private key with sufficient MATIC for gas and USDC for trading. Accessing the Polymtradebot source code is only the first step; you must also secure your environment. We strongly advise against hardcoding these keys directly into the .py files.

- Environment Variables. Store your

PRIVATE_KEYandPOLYMARKET_API_KEYin a.envfile. The bot uses thepython-dotenvlibrary to load these into memory at runtime, keeping your credentials out of the source code and safe from accidental leaks if you use version control. - Polygon RPC URL. Use a dedicated RPC provider rather than public nodes. Public nodes often rate-limit requests, which can freeze your bot during the high-traffic periods common in 5-minute Bitcoin Up/Down markets.

Paper trading and validation

Before deploying changes to a live market, you must use the paper trading mode included in the script. This simulation environment uses real-time market data but executes "ghost" trades. It allows you to verify that your customized logic—such as a new arbitrage calculation for ETH—triggers correctly without risking capital.

Run the bot in simulation for at least 24 hours to observe how it handles liquidity gaps. This step is non-negotiable when moving from established Bitcoin markets to lower-liquidity assets where slippage can eat your margins.

How to customize the bot source code for new markets: Step-by-step

Adapting your underlying architecture ensures the bot performs reliably across diverse regional systems

Adapting your underlying architecture ensures the bot performs reliably across diverse regional systems

Customizing the Polymtradebot source code involves remapping the logic from the default Bitcoin and Ethereum pairs to the specific contract addresses and WebSocket feeds of the target asset. Because Polymarket operates on the Polygon network, every market—whether it is a 5-minute SOL "Up or Down" or a 15-minute XRP prediction—is defined by a unique hex address in the smart contract layer.

Updating asset identifiers

Your first task is to open the constants.py or config.json file in the source directory. This is where the bot stores the MARKET_ADDRESS and TOKEN_ID variables. To swap from Bitcoin to a new SOL market, you must replace the existing contract strings with the specific IDs found in the Polymarket UI or via the Polygonscan block explorer.

If you are targeting a regional or less common market, ensure you capture both the "Binary" (Yes/No) contract address and the underlying collateral token address (usually USDC). Mismatching these will result in failed execution calls when the bot attempts to sign the transaction.

Adjusting execution and data feeds

Once the addresses are set, you need to align the bot's "ears" with the new market's pulse. This requires two specific code modifications:

- WebSocket Stream Handlers. Locate the

ws_handler.pyscript. You must update the subscription payload to pull price data for the new asset (e.g., SOL/USD) instead of BTC/USD. If the new market uses a different price oracle, verify that the data normalization logic matches the decimal precision of that asset. - Asynchronous Patterns. When scaling to multiple markets, use the

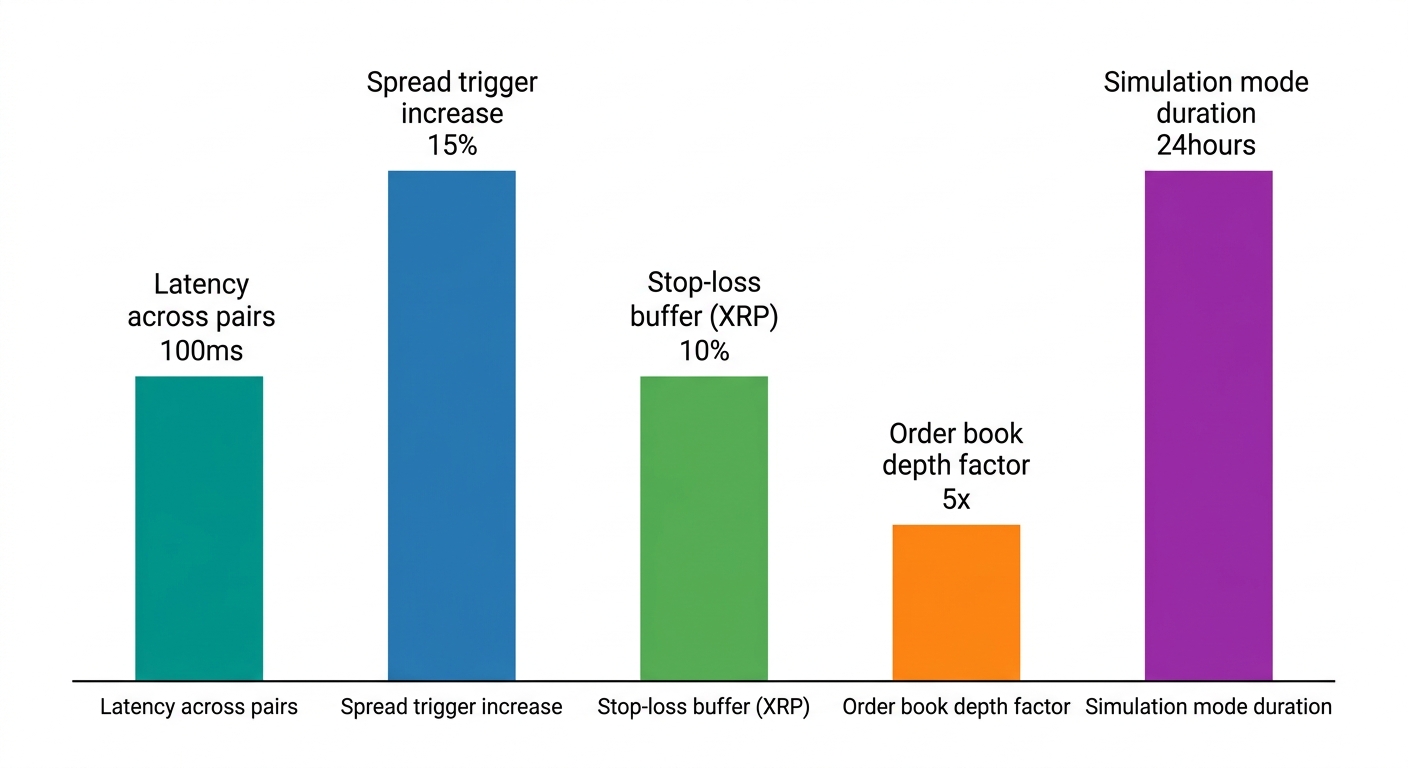

asynciolibrary to manage concurrent streams. By wrapping your market listeners inasyncio.gather(), you prevent the bot from blocking the execution of an ETH trade while it waits for a SOL price update. This keeps latency under 100ms across all active pairs.

Refining strategy parameters

New markets often suffer from thinner order books compared to Bitcoin’s high-liquidity pools. Your arbitrage and execution logic must adapt to these wider spreads to avoid losing your margin to slippage.

Observation. In our practice, we’ve found that transitioning from 5-minute BTC markets to 15-minute SOL markets requires increasing the minimum "spread trigger" by at least 15%. The lower liquidity in altcoin markets often produces "fake" price spikes that can trigger premature entries if your thresholds are too tight.

Updating the risk management module

The final step is hardening the risk_manager.py file. Volatility profiles differ significantly between assets; a 2% swing in Bitcoin is a standard Tuesday, but in a localized or emerging market, it could signal a total liquidity drain.

- Stop-Loss Calibration. Set asset-specific stop-loss limits. For XRP or SOL, we recommend widening the buffer by 10-15% compared to your BTC settings to account for higher "noise" in the price action.

- Dynamic Position Sizing. Modify the code to calculate trade size based on the current order book depth of the new market. If the available liquidity at the top of the book is less than 5x your trade size, the script should automatically scale down the position to prevent self-inflicted slippage.

- Paper Trading Validation. Before deploying to mainnet, run the customized script in the bot's simulation mode for at least 24 hours. This confirms that your new WebSocket handlers and risk triggers are communicating correctly without risking USDC.

Adapting strategies for regional growth

Expanding your trading footprint requires more than just changing a contract address; you must align the bot’s logic with the specific growth trajectories of global markets. By 2026, the Asia-Pacific region is projected to be the fastest-growing chatbot and automated agent market with a 24.71% compound annual growth rate according to Mordor Intelligence. This surge in automation reflects a broader shift: McKinsey research from 2025 indicates that 88% of organizations now use AI in at least one business function to drive growth. For a Polymarket trader, this justifies the move from manual execution to a customized Python script that captures regional volatility while you sleep.

Integrating localized data sources

Standard price oracles often lag during high-impact regional events. To gain an edge in 5-minute Bitcoin or ETH markets, you should integrate localized news sentiment and region-specific price feeds directly into the decision_engine.py file. If you are targeting the Korean or Japanese markets, for instance, the spread on local exchanges (the "Kimchi Premium") can signal an imminent move on Polymarket before the global aggregate price reflects it.

You can modify the source code to fetch data from regional REST endpoints and weight these inputs within your signal generation logic. This prevents the bot from being "blinded" by Western-centric data when trading assets like SOL or XRP during the Asian session.

What we noticed. When running arbitrage strategies between Polymarket and centralized exchanges, a 15-millisecond delay in fetching localized price data can turn a profitable 15-minute trade into a loss due to the rapid convergence of global liquidity.

Capitalizing on Asia-Pacific expansion

Time zone management is a technical requirement, not a logistical one. The liquidity profile of a 5-minute "Bitcoin Up" market at 08:00 UTC (London open) differs drastically from 00:00 UTC (Tokyo open). You need to adjust your order book analysis to account for these shifts. In lower-liquidity windows, the bot should widen its "safety" spread to avoid being stopped out by a single large market order.

Consider these adjustments for regional peaks:

- Liquidity Thresholds. Increase the minimum required volume in the

market_analyzerscript during off-peak hours to avoid slippage. - Volatility Scaling. Use a dynamic multiplier for your risk parameters. In the high-growth Asia-Pacific session, we often see sharper, momentum-driven moves that require tighter trailing stops.

- Ping Optimization. If you are targeting specific regional liquidity, ensure your execution environment (like an AWS instance) is geographically close to the Polygon RPC nodes with the lowest latency for that region.

How to customize the bot source code for new markets effectively involves treating every region as a unique environment with its own "heartbeat." By hardcoding these time-based logic shifts into your Python environment variables, the bot automatically switches from aggressive arbitrage to capital preservation as the sun sets on one market and rises on another.

5 mistakes that break market expansion

Customizing the Polymtradebot source code for new markets requires more than just swapping a contract address. If you treat a low-volume XRP market the same way you treat a high-liquidity Bitcoin pair, the bot will likely execute trades that lose money on the spread alone. Precision in the Python logic prevents these architectural oversights from draining your Polygon wallet.

1. Static liquidity depth checks

Most traders forget to update the liquidity threshold when moving from Bitcoin to smaller altcoin markets. If your script is hardcoded to look for $50,000 in depth before firing an order, it might never trade on a niche 5-minute XRP market. Conversely, if you remove the check entirely, a $500 trade could move the market against you by 2%, resulting in instant slippage that wipes out your projected arbitrage margin.

2. Misaligned expiration logic

Polymarket’s 5-minute and 15-minute markets operate on different settlement rhythms. A common error is using a single expiry_buffer variable across all market types. In a 5-minute "Up or Down" market, being off by 60 seconds represents 20% of the total trade duration. This lag can cause the bot to attempt execution on a market that is already in its "locked" phase, leading to failed transactions and wasted gas fees.

3. Hardcoding fixed price offsets

Using a fixed $0.05 offset for price improvements works for ETH, but it is catastrophic for XRP or SOL. When a token is priced at $0.60, a five-cent offset is a massive percentage of the total value.

Observation. In our practice, we see that successful bots use percentage-based offsets (e.g., 0.1% of spot) rather than nominal dollar values to ensure the strategy remains profitable regardless of the asset's unit price.

4. Bypassing paper trading for regional launches

The temptation to "go live" immediately in a new regional market often leads to ignored edge cases. Different time zones exhibit different volatility patterns; a strategy that works during New York trading hours might fail during the lower-volume periods in the Asia-Pacific region. Running the Polymtradebot in paper trading mode for at least 24 hours allows you to see how the bot handles the specific price feeds and order book density of that new pair without risking capital.

5. Ignoring API rate limits on multi-stream instances

As you scale your Polymtradebot to monitor Bitcoin, ETH, SOL, and XRP simultaneously, you multiply the number of WebSocket subscriptions and REST API calls. Standard API keys often have rate limits (e.g., 100 requests per second). If your customized code doesn't include a centralized rate-limiter or connection pooling, the exchange will throttle your bot precisely when volatility spikes, leaving your positions unmanaged.

Summary of Scaling Risks

| Mistake | Impact | Fix |

|---|---|---|

| Static Depth | High slippage | Dynamic depth based on order size |

| Hardcoded Offsets | Uncompetitive bids | Percentage-based price increments |

| Single Stream | API 429 errors | Asyncio-based request throttling |

| No Simulation | Logic errors | Mandatory 24h paper trading |

Checklist: Verifying your customized deployment

Validation is the only barrier between a profitable strategy and a drained wallet when moving into regional markets like SOL or XRP. Once you have modified the market_constants.py and updated your WebSocket handlers, you must verify that the bot interprets the new environment correctly before enabling live execution.

Connectivity and data integrity

The first step is ensuring your customized script talks to the right endpoints without leaking data or timing out.

- Authentication handshake. Confirm the bot successfully authenticates with the Polymarket proxy using your new asset IDs. Check the logs for a

200 OKresponse specifically tied to the new contract addresses; a generic connection success doesn't guarantee the bot can place orders in that specific niche. - Stream stability. Verify that the WebSocket stream receives real-time updates for the new market without drops. In 5-minute markets, a 10-second lag is a lifetime. Monitor the heartbeats to ensure the connection stays pinned during high-volatility periods common in the Asia-Pacific trading sessions.

- Latency benchmarks. Validate that automated execution triggers within the expected 200–500ms latency window. If the regional node you are hitting adds significant round-trip time, you may need to adjust your gas settings on the Polygon network to prioritize transaction inclusion.

Logic and risk assessment

Customizing for new assets often changes the underlying math of your strategy, particularly regarding liquidity and tick size.

- Liquidity-adjusted position sizing. Ensure the risk management module correctly calculates position sizes based on the new market's depth. If you are moving from Bitcoin to XRP, the order book is likely thinner. The bot must downsize orders to avoid eating the spread and ruining your ROI.

- Paper trading fidelity. Check that the paper trading logs reflect the intended strategy execution for the customized parameters. We recommend running the bot in simulation mode for at least one full 24-hour cycle to capture the liquidity shifts between different global time zones.

What we noticed. When shifting from 15-minute ETH markets to 5-minute SOL markets, the most common failure point isn't the code logic, but the price oracle frequency. If your external price feed updates slower than the Polymarket order book, the bot will constantly chase "ghost" arbitrage opportunities that have already closed.

Final execution audit

Before you flip the switch to live trading, perform a final check of the execution environment variables.

- Environment Variable Check: Confirm that

POLYGON_RPC_URLandPRIVATE_KEYare loaded from the.envfile and not hardcoded, ensuring you aren't accidentally using a testnet key for a mainnet market. - Contract Address Mapping: Cross-reference the Polymarket API documentation to ensure the

conditionIdin your code matches the specific "Up" or "Down" outcome for the new asset. - Slippage Tolerance: Verify the

max_slippagevariable is scaled. A 0.5% slippage limit might work for Bitcoin but could prevent all fills in a less liquid XRP market, effectively idling your bot.

If the logs show consistent price updates and the paper trading balance moves in line with your backtested expectations, the deployment is ready for localized liquidity.

Conclusion

Customizing the Polymtradebot source code allows you to transition from standard 5-minute Bitcoin markets to niche assets like SOL or XRP. Success relies on precise contract mapping and adjusting your strategy parameters to match the liquidity of the new environment. By following a structured modification process, you ensure the bot executes trades based on accurate regional data rather than generic defaults.

Effective expansion requires more than just changing a ticker symbol. You must recalibrate risk management thresholds and verify execution speeds to maintain an edge in competitive arbitrage. Testing these changes in paper trading mode first prevents costly errors during the initial deployment phase.

Review the latest strategies on our blog to see how specific code adjustments perform in live 15-minute markets. You can also compare different setup tiers on our pricing page to find the right configuration for your scaling needs.

FAQ

Can I use the same API key for multiple regional markets?

Yes, a single Polymarket API key works across different regional markets because it is tied to your underlying wallet and the Polygon network. However, you must manage your rate limits carefully if you run multiple bot instances simultaneously. Exceeding the standard request threshold can lead to temporary IP bans or missed execution windows in high-volatility periods.

How do I find the specific contract addresses for new Polymarket assets?

You can find contract addresses by inspecting the "Activity" or "Market Details" section on the Polymarket interface or by querying the Polymarket API documentation. Every market, such as a 5-minute Bitcoin Up/Down event, has a unique identifier. Ensure you copy the exact Proxy or Condition ID into your Python script to avoid sending orders to the wrong pool.

Is it necessary to rewrite the arbitrage logic for every new market?

No, the core arbitrage logic remains functional across different assets like ETH or SOL, but you must adjust the spread sensitivity. Different markets have varying bid-ask widths and liquidity depths. While the mathematical formula stays the same, you should update the minimum profit threshold in your config file to account for the specific slippage typical of that asset.

What are the risks of using the paper trading mode for simulation in low-liquidity markets?

Paper trading often fails to account for market impact, meaning it assumes your large orders won't move the price. In low-liquidity XRP or niche markets, a real trade might trigger significant slippage that the simulation ignores. This can lead to "profitable" backtests that actually lose money in live execution due to the gap between theoretical and actual fill prices.

How does latency optimization differ when targeting markets in different geographical regions?

Latency optimization focuses on the physical distance between your hosting server and the Polygon RPC nodes rather than the "region" of the bet. Since Polymarket is decentralized, you gain the most speed by using private RPC providers with nodes located in major data hubs. Reducing this round-trip time is critical for 5-minute markets where a 200ms delay can result in a rejected order.

Sources

- Mordor Intelligence (2026) — By 2026, the Asia-Pacific region is projected to be the fastest-growing chatbot market with a 24.71% compound annual growth rate.

- Gartner (2025) — Gartner predicts that by 2026, 40% of enterprise applications will feature task-specific AI agents, up from less than 5% in 2025.

- McKinsey & Company (2025) — McKinsey research from 2025 indicates that 88% of organizations now use AI in at least one business function to drive growth.