Between April 2024 and April 2025, arbitrage traders extracted approximately $40 million in profits from Polymarket by exploiting pricing inefficiencies, according to research by the IMDEA Networks Institute published in 2025. This massive figure highlights a fundamental reality: prediction markets rarely move in perfect sync with global spot prices. When Bitcoin or Ethereum spikes on Binance, the "Yes" shares in a Polymarket 5-minute price candle often lag by several seconds. If you are manually clicking buttons, you are already too late to capture the spread. Success in this environment requires understanding exactly how automated arbitrage works on Polymarket to bridge the gap between external data feeds and on-chain execution.

You will learn how to structure a high-frequency trading architecture that monitors real-time feeds for Bitcoin, ETH, SOL, and XRP to identify these mispriced shares. We break down the technical requirements for maintaining a sub-3-second execution loop and why bot-driven liquidity is the primary force moving these markets. By the end of this analysis, you will have a clear blueprint for deploying Python-based scripts that manage risk through paper trading simulations before committing capital to live arbitrage strategies. This approach moves you away from speculative betting and toward a systematic process of capturing mathematical discrepancies.

Table of contents

- The mechanics of prediction market arbitrage

- Components of an automated trading architecture

- The 2.7-second window for execution

- Why bot dominance shapes market liquidity

- Arbitrage strategies for Bitcoin and ETH markets

- Risk management in automated prediction trading

- Checklist: Verifying bot performance and safety

- The Shift Toward Systematic Execution

- FAQ

- Sources

The mechanics of prediction market arbitrage

Bots execute rapid trades to capture price differences between Polymarket and external data feeds

Bots execute rapid trades to capture price differences between Polymarket and external data feeds

Automated arbitrage on Polymarket functions by identifying price gaps between a market's "Yes" or "No" shares and the real-time spot price of the underlying asset on centralized exchanges. In 2025, the IMDEA Networks Institute found that traders extracted 40 million dollars in profit by exploiting these inefficiencies. While a standard exchange like Binance reflects the immediate price of Bitcoin, Polymarket reflects the collective probability of a specific outcome, such as "Bitcoin above $70,000 at 4:00 PM." When the spot price moves faster than the prediction market participants can react, an arbitrage window opens.

Defining the price gap

The gap exists because Polymarket shares are binary options. If you buy a "Yes" share for $0.60, the market is pricing a 60% probability of that event occurring. If Bitcoin’s spot price surges on Coinbase, the "true" probability of a "Bitcoin Up" outcome might instantly jump to 80% ($0.80), but the Polymarket order book may still have sell orders sitting at $0.65.

Automated scripts detect this $0.15 discrepancy and execute the trade before the manual crowd adjusts. According to Yahoo Finance, these arbitrage windows compressed from 12.3 seconds in 2024 to an average of 2.7 seconds by late 2025. This speed requirement makes manual trading nearly impossible for arbitrage; if you aren't using a bot, you are the liquidity being harvested.

The role of conditional tokens

Polymarket operates on the Polygon blockchain using the Conditional Token Framework. When you enter a trade for Bitcoin or ETH, you aren't buying the coin itself. You are interacting with a smart contract that holds collateral in escrow.

- Minting: The contract splits 1 USDC into one "Yes" token and one "No" token.

- Settlement: Upon market expiry, the contract queries an oracle—usually Chainlink—to verify the asset's price.

- Payout: The smart contract automatically devalues the losing tokens to $0 and moves the full collateral to the winning tokens, making them redeemable for $1.00.

What we noticed. In the 5-minute Bitcoin "Up or Down" markets, the most profitable arbitrage doesn't happen at the start of the window, but in the final 30 seconds before expiry when the oracle feed and the share price must converge.

Because these outcomes are bound by smart contracts, the settlement is deterministic. There is no counterparty risk regarding the payout; the "risk" in the arbitrage lies entirely in the execution speed and the gas fees required to land the transaction within that 2.7-second window. At Polymtradebot, we focus our Python scripts on these high-velocity assets like BTC, ETH, and SOL because their high trading volume ensures the order books are deep enough to absorb arbitrage entries without immediate slippage.

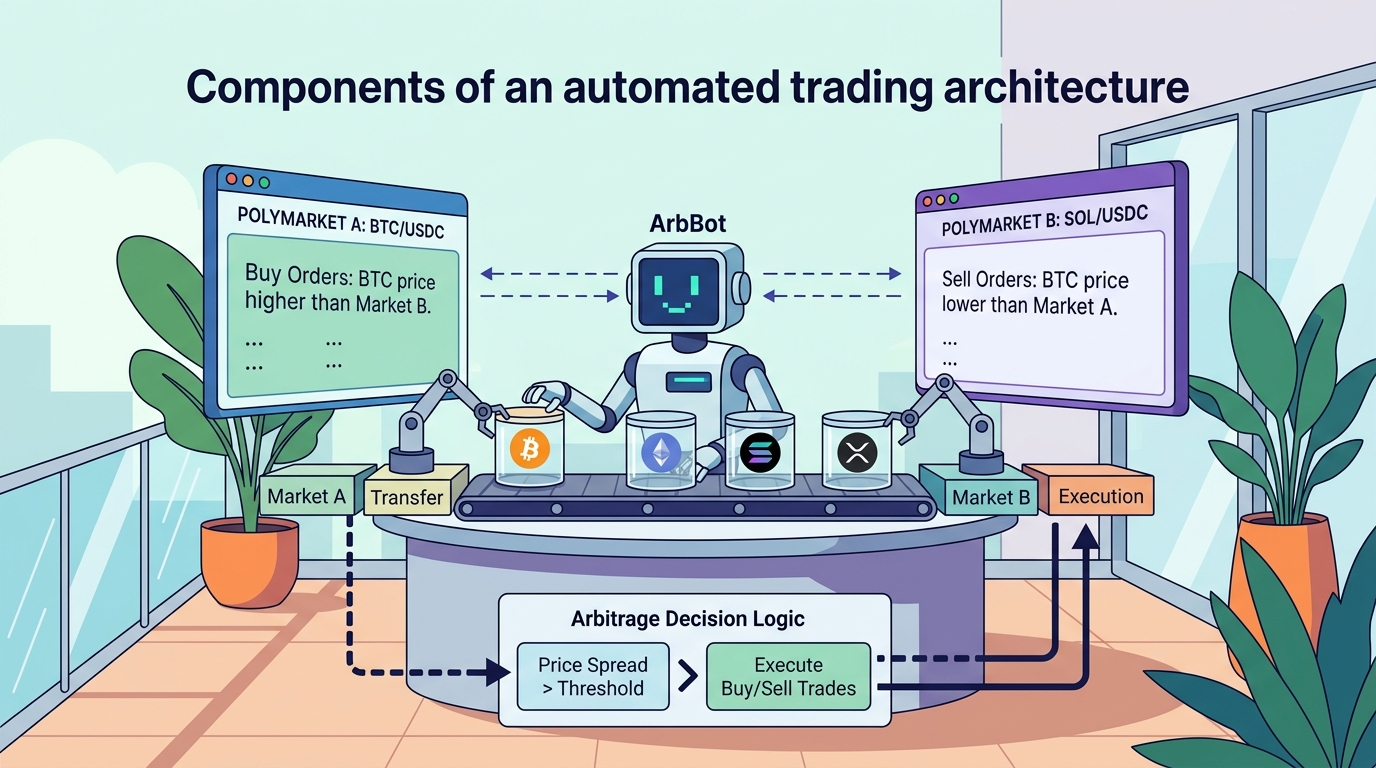

Components of an automated trading architecture

Efficient execution relies on seamlessly connecting data feeds to the order execution engine

Efficient execution relies on seamlessly connecting data feeds to the order execution engine

To capture the inefficiencies identified by researchers at the IMDEA Networks Institute in 2025, your infrastructure must bridge the gap between centralized exchange data and decentralized settlement. A functioning bot isn't just a script; it is a high-speed pipeline that moves data from a price source to a smart contract in milliseconds.

Real-time data ingestion

The foundation of any arbitrage bot is a low-latency connection to both the prediction market and external price feeds. In our development of Polymtradebot, we focus on WebSocket connections rather than standard REST API polling. Polling creates a "stale data" lag; WebSockets push every order book update to your script the moment it happens.

For 5-minute and 15-minute Bitcoin markets, the bot must monitor the "order book depth"—the volume of Yes/No shares available at various price points. If a large trader dumps shares and moves the Polymarket price to $0.52 while the real-world probability (based on Binance or Coinbase spot prices) implies $0.55, the bot has a fleeting window to buy the discount.

Execution logic and external feeds

The "brain" of the architecture is a Python-based engine that runs a continuous comparison loop. It ingests price data for Bitcoin, ETH, SOL, or XRP from major global exchanges and calculates the "fair value" of a Polymarket share.

- Signal Triggering: When the spread between the external price and the Polymarket share price exceeds your pre-set threshold (accounting for gas and trading fees), the script triggers an execution signal.

- Paper Trading Mode: Before risking capital, we use a simulation layer. This allows you to test how the bot would have handled a 5-minute Bitcoin "Up" market volatility spike without actually moving funds on-chain.

- Automated Execution: Once live, the script interacts with the Polymarket matching engine via the Polygon network. It must handle private key management and transaction signing locally to ensure the trade hits the book before the 2.7-second arbitrage window closes.

Observation. In our practice, the most successful scripts don't just look at the current price; they monitor the "depth of book" on both sides to ensure there is enough liquidity to exit the position profitably if the market moves against the bot.

High-frequency infrastructure

Running a bot on a home laptop is a recipe for slippage. High-frequency trading in a decentralized environment requires a Virtual Private Server (VPS) located near the primary API endpoints. This minimizes network "hops." Because Polymarket settles on Polygon, your architecture also needs a dedicated RPC (Remote Procedure Call) node. Public nodes are often rate-limited or slow, which can lead to failed transactions during high-traffic events like a Bitcoin price breakout.

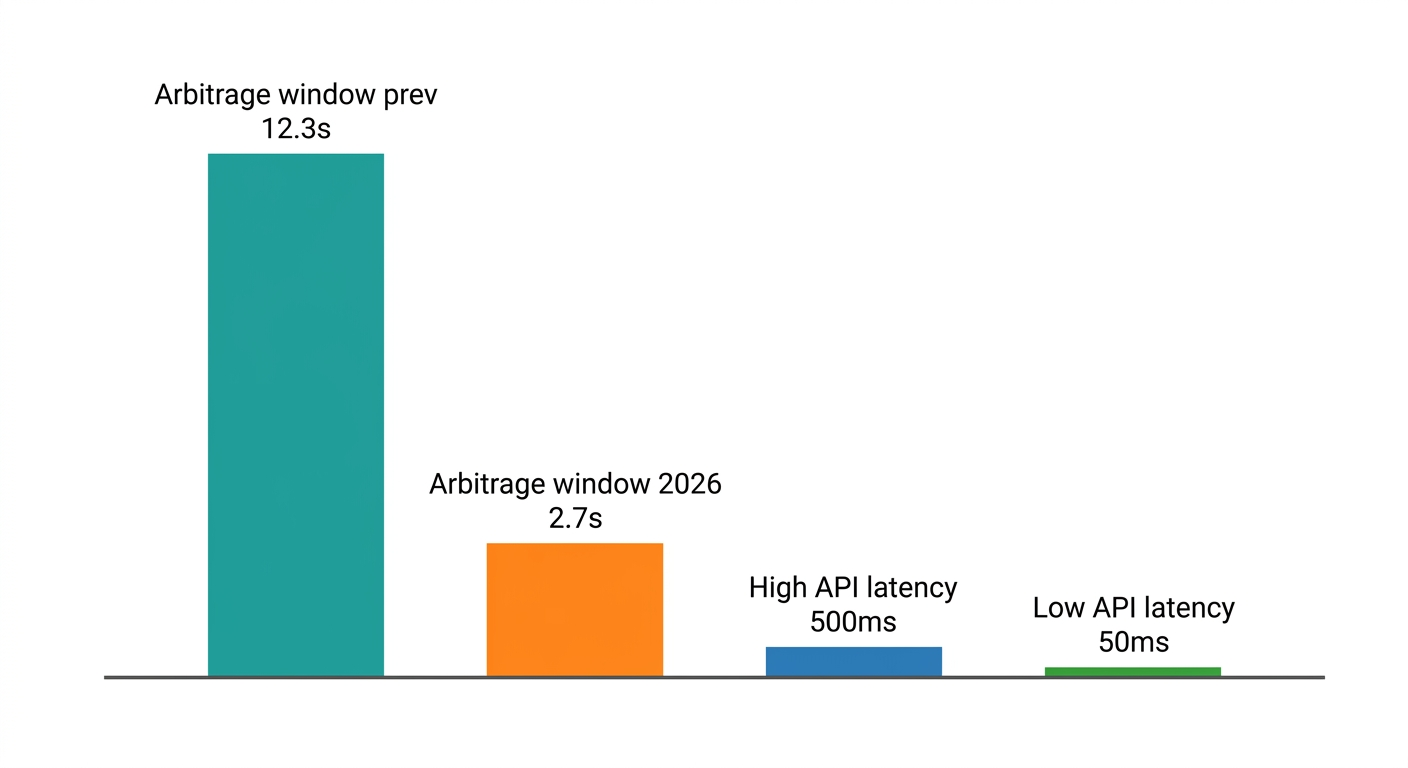

The 2.7-second window for execution

Speed and precision are critical for capturing fleeting price gaps before markets adjust

Speed and precision are critical for capturing fleeting price gaps before markets adjust

The speed of the prediction market has moved beyond human reaction times. According to a Yahoo Finance 2026 report, the average arbitrage window on platforms like Polymarket has compressed from 12.3 seconds to just 2.7 seconds. If you aren't executing within this sub-3-second frame, the price discrepancy between the internal market and external feeds like Binance or Coinbase has already been closed by a bot.

Latency compression and the race for block space

Capturing alpha on Polymarket isn't just about spotting a price difference; it’s about winning the race to the next block. When a 5-minute Bitcoin market lags behind a sudden price spike on a spot exchange, dozens of scripts identify the gap simultaneously. The winner is the one whose transaction is indexed first by the Polygon network.

In our practice at Polymtradebot, we’ve seen that network congestion can spike API latency from 50ms to over 500ms in seconds. During these high-traffic periods, manual traders are essentially locked out. While a human is still moving their mouse to click "Buy Yes," an automated script has already calculated the optimal position size, adjusted for slippage, and broadcast the transaction.

Observation. In the 15-minute ETH markets, we frequently see arbitrage opportunities vanish in exactly one block cycle (roughly 2 seconds), meaning any execution logic requiring manual confirmation is mathematically certain to fail.

Why manual trading is unviable

The shift to a 2.7-second window changes the fundamental nature of trading on the platform. Manual execution introduces three points of failure that bots bypass:

- Visual Latency. The time it takes for a browser to refresh the order book UI and for your eyes to register the change.

- Decision Fatigue. A bot maintains the same execution logic at 3:00 AM as it does at noon, whereas human precision drops during volatile sessions.

- Transaction Signing. Manually confirming a wallet pop-up adds 1–2 seconds of overhead—often the entire duration of the arbitrage window.

For markets like XRP or SOL, where price movements can be jagged, the risk of "getting picked off" increases for manual traders. You might enter a trade based on a price you saw two seconds ago, only to find the market has already moved against you, turning a potential arbitrage gain into an instant loss. Automated execution via Python scripts removes these bottlenecks by interacting directly with the Polygon protocol and Polymarket’s CLOB (Central Limit Order Book) API. This ensures that when the script sees a 2.7-second window, it occupies it immediately.

Why bot dominance shapes market liquidity

The shift from manual to automated trading on Polymarket isn't just a trend; it is a structural takeover. A Bloomberg 2026 analysis highlights this reality, revealing that 14 of the top 20 most profitable wallets on the platform are bots. These automated systems don't just extract value; they provide the foundational liquidity that allow 5-minute and 15-minute Bitcoin and ETH markets to function without massive price swings.

Profitability of automated wallets

Sophisticated algorithmic traders dominate the leaderboard because they eliminate human hesitation. While a retail trader might spend 30 seconds calculating the implied volatility of a "Bitcoin Up" contract, a bot executes the trade in milliseconds. This speed allows bots to capture the spread between the prediction market and external spot prices before the window closes.

The concentration of profits among these wallets stems from their ability to run 24/7 across multiple pairs. By using Python scripts like Polymtradebot, traders can monitor Bitcoin, SOL, and XRP feeds simultaneously. This creates a high-frequency environment where the most efficient code—not the most "correct" opinion—earns the highest yield.

The impact on retail participants

For the average user, bot dominance is a double-edged sword. On one hand, bots act as permanent market makers. Their constant bid-ask activity ensures that when you want to buy a "Yes" share for a Bitcoin price move, there is a seller available at a fair price. This liquidity provision significantly reduces price slippage, meaning you get a fill price closer to the actual market value.

Observation. In our practice with 5-minute Bitcoin markets, we’ve seen that liquidity clusters around bot-heavy execution zones, narrowing the spread by up to 40% compared to less automated niche markets.

However, this creates a feedback loop that rewards efficiency over intuition. As automated volume increases, the market becomes more efficient, leaving fewer "easy" wins for manual traders. The price discrepancies that used to last for minutes now disappear in the 2.7-second execution window.

The result is a market where liquidity is deep, but the barrier to entry for profitability has moved from "having a good hunch" to "having a faster script." This environment makes paper trading mode essential for anyone transitioning to automated execution, as it allows you to test how your strategy competes against the existing bot landscape without risking capital.

Arbitrage strategies for Bitcoin and ETH markets

Profitable arbitrage on Polymarket relies on the speed at which a bot can reconcile the "Yes" share price of a prediction market with the underlying spot price of assets like Bitcoin or ETH. Because Polymarket outcomes are binary—settling at either $1.00 or $0.00—the fair value of a share is essentially the probability of the event occurring. If Bitcoin is trading at $64,950 on Binance and a "Bitcoin above $65,000" 5-minute market on Polymarket is priced at $0.10 (implying a 10% chance), a sudden $40 spike in spot price should instantly recalibrate that share price.

Cross-exchange price alignment

Bots maintain a constant websocket connection to high-liquidity exchanges to predict market outcomes before the Polymarket order book reacts. When the spot price of Bitcoin or SOL moves toward a strike price, the bot calculates the new theoretical probability. If the external price suggests a 70% probability but Polymarket shares are still trading at $0.62, the bot executes a buy order to capture the 8-cent discrepancy.

To lock in these returns without directional risk, we often use a hedging layer. This involves taking an offsetting position on a perpetual futures platform. For every "Yes" position bought on Polymarket, the bot opens a short position of equivalent size on the underlying asset. This setup ensures that if the market moves against the "Yes" bet, the gain on the short position offsets the loss, leaving the trader with the captured arbitrage spread as profit.

Handling high volatility in ETH and XRP

ETH and XRP markets often exhibit different volatility signatures than Bitcoin. During major network upgrades or SEC litigation updates, XRP liquidity can thin out, leading to wider spreads between the bid and ask. Our Python scripts at Polymtradebot monitor these depth changes to prevent the bot from entering trades where slippage eats the entire arbitrage margin.

In high-volatility events, ETH markets frequently "over-correct." If a sharp drop occurs, the prediction market often overshoots the probability of a "Down" outcome. Bots programmed for mean reversion identify when the "No" shares are underpriced relative to the speed of the price recovery, allowing for quick entries and exits within the 5-minute or 15-minute windows.

What we noticed. In the 15-minute XRP markets, price discrepancies often linger 1.5 seconds longer than in Bitcoin markets due to lower bot density, providing a higher success rate for scripts with optimized latency.

Simulation through paper trading

Before committing capital to live markets, you should use the paper trading mode. This simulation environment mirrors the live order book and external price feeds without executing real transactions. It allows you to:

- Test latency impact: Observe if your execution speed is sufficient to beat competitors to the 2.7-second window.

- Refine thresholds: Determine the minimum price discrepancy (e.g., 1.5% vs 2%) required to cover transaction fees and still net a profit.

- Stress test volatility: See how the bot handles "flash" movements in SOL or ETH where the oracle feed might lag behind the spot price.

Using this data-driven approach ensures that when you move to live execution, the strategy is tuned to the specific liquidity profiles of the 5-minute and 15-minute cycles.

Risk management in automated prediction trading

Automated systems must treat Polymarket not just as a prediction venue, but as a high-velocity execution environment where liquidity can vanish in milliseconds. While the 2.7-second execution window defines the opportunity, risk management defines the longevity of the bot. Without rigorous controls on slippage, position sizing, and oracle latency, a single volatile event in Bitcoin or ETH can wipe out weeks of arbitrage gains.

Slippage protection and execution logic

Bots calculate maximum allowable price slippage by comparing the mid-market price on Polymarket to the real-time feed from an external exchange like Binance or Coinbase. If the spread is 2% but the order book depth suggests your buy order will push the price up by 1.5%, the net profit shrinks to 0.5% before fees.

To prevent "buying the top" of a thin market, we program scripts to set a hard slippage cap—typically 0.1% to 0.3% for 5-minute Bitcoin markets. If the execution price exceeds this threshold during the transaction broadcast, the bot cancels the order immediately. When handling partial fills in thin order books, the system evaluates the remaining "leave" quantity; if the remaining shares no longer offer an arbitrage margin, the bot kills the rest of the order rather than chasing a bad price.

Capital allocation and stop-loss logic

Effective arbitrage isn't about betting the bank on one 15-minute window. It’s about high-frequency, low-exposure cycles. We implement position sizing based on a percentage of the total principal—often limiting any single outcome to 2-5% of the wallet. This ensures that even a "black swan" event where an oracle settles against the price feed doesn't cause a catastrophic drawdown.

Observation. In our practice, we’ve seen that 5-minute markets are highly sensitive to "fat tail" events where a single large manual trade spikes the price. Our bots are configured to pause for 30 seconds if they detect a price move exceeding 3 standard deviations from the 1-minute mean, preventing the system from entering a volatile "noise" trap.

Managing oracle and data risks

Because Polymarket relies on decentralized oracles (like the UMA Optimistic Oracle), there is a structural risk of delayed data reporting or disputed outcomes. An automated system must account for:

- Feed Latency: If the bot's Python script sees a Bitcoin price move but the Polymarket API hasn't updated its order book, the bot must verify the "freshness" of the market data before firing.

- Oracle Disputes: While rare, if an outcome is disputed, capital remains locked. Automated systems should maintain a "liquidity buffer" to continue trading other markets while a dispute is resolved.

- Network Congestion: On-chain execution can fail if gas prices spike. We use dynamic gas fee estimation to ensure our arbitrage trades are included in the next block, avoiding the "stale trade" risk where a transaction confirms after the arbitrage window has already closed.

By treating every trade as a statistical probability rather than a certainty, Polymtradebot users can run simulations in paper trading mode to stress-test these limits against historical volatility before committing live capital.

Checklist: Verifying bot performance and safety

You cannot trust an arbitrage strategy until you have stress-tested the execution logic against the volatile reality of the Polymarket order book. High-frequency trading requires more than a functional script; it demands a system that handles 200ms latency spikes and API timeouts without draining your wallet. Before deploying capital into the 5-minute Bitcoin Up or Down markets, use this checklist to audit your setup.

Backtesting and Simulation

Verify the robustness of your Python trading bot script by running it against historical Polymarket data and external price feeds from 2025 and early 2026. A script that looks profitable in a vacuum often fails when you factor in the 0.1% to 0.5% slippage common in thinner markets like XRP or SOL.

- Paper Trading. Use the paper trading mode in Polymtradebot to simulate live execution. This allows you to see how the bot reacts to the 2.7-second arbitrage windows identified in recent market reports without risking principal.

- Historical Replay. Run your logic against past high-volatility events—such as a $2,000 Bitcoin price swing within ten minutes—to see if your stop-loss and slippage parameters trigger correctly.

- Latency Simulation. Artificially delay your outgoing orders by 500ms during testing. If the bot still captures alpha, your strategy is resilient; if the profit evaporates, you need to optimize your connection or find wider spreads.

Execution Logs and Error Handling

Transparent logging is your only defense against "ghost" trades or silent failures. If a trade fails because of a gas spike on the Polygon network or a timeout from a price oracle, you need to know exactly why within seconds.

- Granular Logs. Ensure your bot logs every step: price fetch, signal generation, order submission, and transaction hash confirmation.

- Error Recovery. Audit the script’s ability to "self-heal." If the API disconnects, the bot should attempt a reconnection sequence rather than crashing and leaving a position unhedged.

- Slippage Protection. Confirm the bot rejects trades if the price moves beyond your limit between the time the signal is generated and the transaction hits the block.

Observation. We noticed that bots failing to account for "partial fills" often leave traders with unbalanced books. In our 15-minute ETH market tests, ensuring the bot immediately recalculates the remaining hedge after a partial fill was the difference between a 2% daily gain and a break-even session.

Security and API Management

Your API keys and wallet permissions are the most vulnerable points in your architecture. Automated arbitrage requires a hot wallet, but that doesn't mean you should leave the door open.

- Scope Permissions. When generating API keys on external exchanges for price feeds, disable "Withdrawal" permissions. The bot only needs "Read" and "Trade" access.

- Environment Variables. Never hardcode your private keys or API secrets directly into the Python script. Use a

.envfile or a dedicated secret manager to keep sensitive data out of your code repository. - Wallet Isolation. Use a dedicated trading wallet for Polymarket rather than your primary storage address. Only keep the capital required for your active arbitrage cycles in the bot-controlled wallet to limit exposure in case of a local system compromise.

The Shift Toward Systematic Execution

Arbitrage on Polymarket has evolved from a manual hustle into a high-frequency race. Success no longer depends on spotting a price gap, but on the technical ability to close it before the order book rebalances. By moving from manual clicks to automated Python scripts, you eliminate the emotional hesitation that often leads to "slippage" in fast-moving 5-minute Bitcoin markets.

Our experience with Polymtradebot shows that the most consistent returns come from managing the spread between Polymarket and spot exchanges like Binance. We focus on the 2.7-second execution window because that is where the most significant price discrepancies live. If your setup can't react within that timeframe, you aren't trading arbitrage; you're just gambling on the next price tick.

What we noticed. In the 5-minute "Bitcoin Up/Down" markets, price gaps larger than 2% typically vanish in under four seconds, making manual execution mathematically inferior to even a basic API script.

Refine your strategy by testing these mechanics in a risk-free environment. You can use the paper trading mode on https://polymtradebot.com to validate your logic against live market data before committing capital to the liquidity pool.

FAQ

How does network latency affect arbitrage profitability on Polymarket?

Network latency determines whether your transaction reaches the Polygon blockchain before a competitor's. A delay of even 500 milliseconds can result in a failed trade or a lower profit margin because the price gap has already narrowed. Profitable bots minimize this by using dedicated RPC nodes rather than public endpoints to ensure faster block inclusion.

Can automated bots trade on both 5-minute and 15-minute Bitcoin markets?

Yes, bots can simultaneously monitor and execute trades across multiple timeframes and assets like BTC, ETH, and SOL. Automated scripts use asynchronous loops to track the 5-minute and 15-minute markets in parallel, identifying arbitrage opportunities that human traders would miss while switching tabs. This multi-market coverage is essential for maintaining high capital utilization.

What is the difference between paper trading and live execution for arbitrage?

Paper trading simulates execution using real-time data without risking actual funds, while live execution interacts directly with the Polymarket smart contracts. In our practice, paper trading is used to calculate the "theoretical yield" and check for logic errors in the Python script. Live execution adds the variables of gas fees, slippage, and actual order book depth.

Why are most of the profitable wallets on Polymarket identified as bots?

Bots dominate the leaderboards because they can maintain 24/7 uptime and execute trades with millisecond precision. Humans cannot compete with the speed required to capture micro-inefficiencies in the 5-minute Bitcoin Up or Down markets. Most top-tier traders use automated scripts to manage risk, hedge positions, and hit limit orders the instant a price target is met.

What programming languages are typically used for Polymarket trading scripts?

Python is the standard language for Polymarket bots due to its extensive libraries for data analysis and blockchain interaction. Developers use the Web3.py library to connect to the Polygon network and handle transaction signing. While some high-frequency shops use C++ or Rust for extreme speed, Python provides the best balance of development speed and execution performance for most arbitrageurs.

Sources

- IMDEA Networks Institute (2025) — Arbitrage traders extracted approximately $40 million in profits from Polymarket between April 2024 and April 2025 by exploiting pricing inefficiencies.

- Yahoo Finance (2026) — Automated arbitrage windows on Polymarket compressed from 12.3 seconds in 2024 to an average of 2.7 seconds by late 2025.

- Bloomberg (2026) — Analysis of Polymarket trade records since early 2025 shows that 14 of the top 20 most profitable wallets are bots.